A Dealmaking Default Fit for a Playground

As complex as it may seem at first glance, the indie film world's "50/50 Pools Waterfall" gets its power and flexibility by capturing a childlike sense of intuitive fairness.

The best deals — the ones that close relatively quickly and smoothly, and leave both sides feeling equally happy (rather than equally unhappy) at the end — often have one key thing in common: a smart eight-year-old could understand why they make sense.

I call this the “playground fairness” rule: when faced with a range of reasonable positions I could take in a negotiation, none of which seems obviously superior to any other, I generally favor whichever option is easiest to explain and defend — initially to my counterpart, but implicitly to the client they represent — as being intuitively fair and equitable.

Among the many problems with pure “positional bargaining” is that it can go on pretty much forever, limited only by the patience, stamina, and shamelessness of the parties and their representatives.1 The parties know they’re done when they’ve run out of middle ground or are simply too exhausted to continue. But when presented with a position that is well-grounded in basic fairness and intuitive justice, countering it implicitly requires (1) a persuasive argument for why it isn’t actually fair, (2) a specific alternative that can be presented as “more” fair, and/or (3) the willingness to openly violate a powerful and near-universal social norm (that is recognized by, and imposes social pressure upon, even those who don’t personally subscribe to it). If the other side can’t muster any of those three things, then they have little choice but to accept the outcome and move on.

The point here isn’t to be nice (or lazy), even if it means “leaving value on the table” or “giving away the store” — it’s to expedite closing the deal by trying to box my counterpart into an outcome that I know I can be comfortable with, when considering the deal holistically. Allow me to illustrate with an example from just last month:

An indie film producer I work with sought my advice on a deal with a buzzy writer/producer, who my client wanted to partner with on a proposed feature, but who was insisting upon a 75/25 split (in the writer’s favor) of the TBD total available producing fees and backend for the project.2 My client acknowledged that the writer’s name recognition and “cool factor” would be essential to the project’s success. But he didn’t feel great about accepting a minority share of the fees, given how accommodating he had been about paying out-of-pocket for a script — at 200% of normal scale, thanks to the writer working with two of his (non-famous) friends, who would also piggyback on the writer as producers — rather than pushing them to work on spec as so many other indie producers are wont to do. And it didn’t help that my client would have to split his fees and backend 50/50 with a silent partner (who was putting up the money for the writing deal).

But after a few rounds, my client was ready to begrudgingly concede that the deal would never close with the pure 50/50 split that he had contemplated, and now wanted my feedback on his plan to go back with an offer of a 55/45 split. I suggested he should instead offer a more generous 60/40 split. Why? There were actually five parties at the table, not two — my client had his silent partner, and the buzzy writer had his two friends. A “60/40” split was, in reality, a 20/20/20/20/20 split. Kind of hard to argue with that. But I also suggested he limit that 60/40 split to the (higher upside, but much more speculative) backend compensation only, and hold at a 50/50 split of the front-end fees (which would be more meaningful and satisfying to my client and his partner, and could be justified exactly as it had been explained to me).

At this point, you may be wondering…

Isn’t This Supposed to Be About the 50/50 Pools Waterfall We Learned About on Monday?

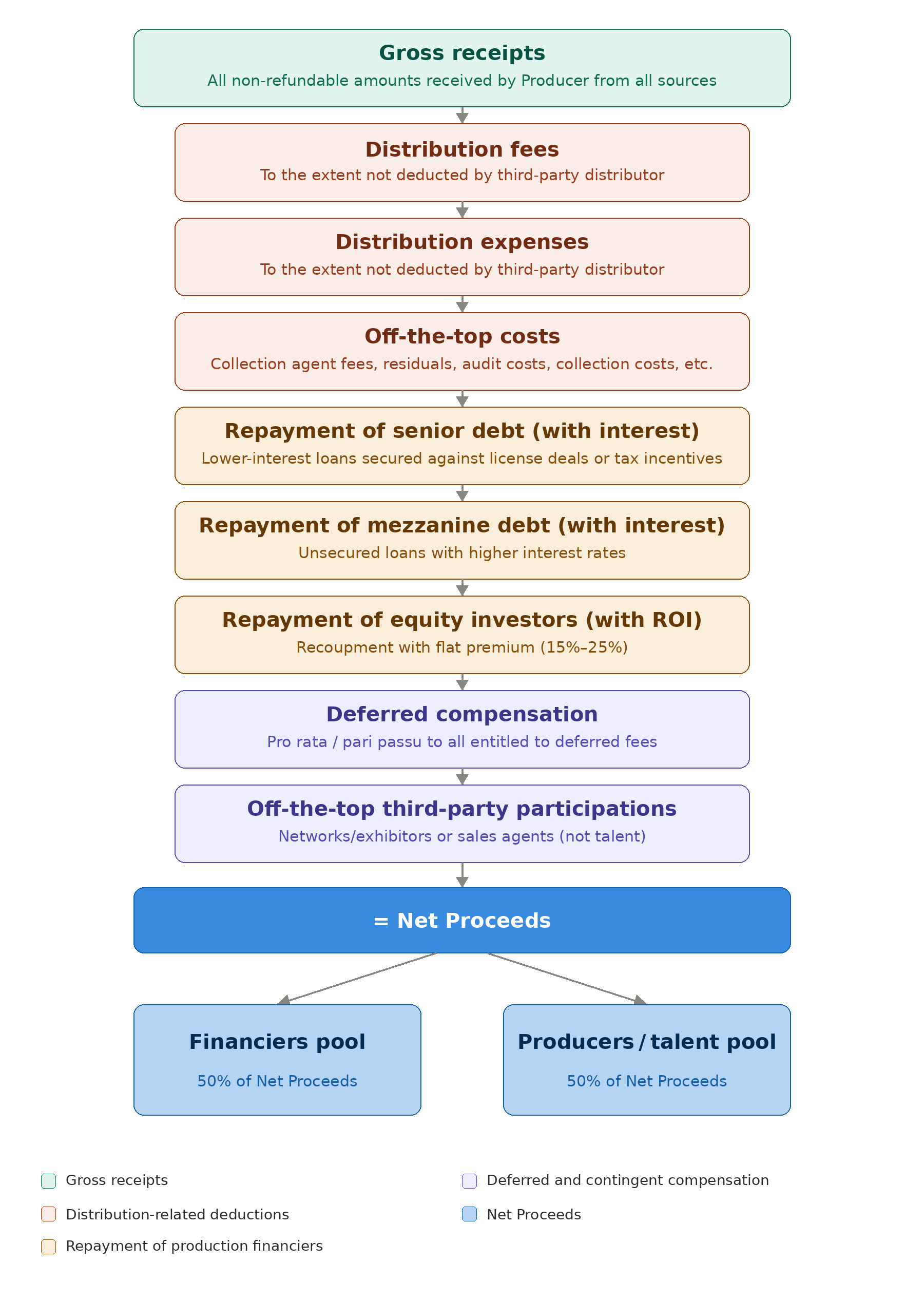

Yes, I’m getting there. It’s easy to look at the 50/50 Pools Waterfall and just see a complicated accounting construct that only a lawyer could love:

But you can start to appreciate how it passes the “playground fairness” test if you simplify it to six brief statements:

Money goes in.

Distributors take their fees and expenses off the top.

Loans are repaid to lenders with interest.

Equity investors recoup their investments with a reasonable premium.

Once those who risked money have been taken care of, those who agreed to be badly “underpaid” to get the project produced are made closer to whole.

Whatever remains goes half to the equity investors whose money made the project possible, and half to the people whose effort and talent made it worthwhile.

Why Does the 50/50 Pools Waterfall Feel Intuitively Fair?

At this point, you’re probably starting to feel the basic logic and equity there, even if you can’t yet put your finger on exactly why you’re feeling it. So let’s look at exactly what makes this model so appealing.

Keep reading with a 7-day free trial

Subscribe to The Business of Television Max(+) to keep reading this post and get 7 days of free access to the full post archives.